As Kraft Foods Group CEO Tony Vernon reminded analysts and investors last fall (click here), volumes in many US ‘center of store’ categories are at best flat, or at worst in terminal decline, while a “weak economy with highly volatile commodity prices is now the new normal”.

He added: “What’s most worrisome is that no-one, absolutely no-one, has grown volume over the time period - that has to change and Kraft must lead that change.”

Growth opportunities at home

For Vernon, who stands at the helm of an $18.7bn packaged foods giant boasting brands including Maxwell House, Oscar Mayer, Kraft, Planters and JELL-O, the only way to grow in this environment is via innovation, operational excellence and better brand building.

At ConAgra Foods, meanwhile, the recipe for growth lies in unlocking the growth potential in the US private label market, driving innovation in frozen food, and growing its presence in sexier categories from pita chips and breakfast sandwiches to packaged fruit.

Other firms such as Coca-Cola are placing their bets on innovative new brands tapping into growing health and wellness trends (Honest Tea, Zico, Core Power, NOS Energy), while General Mills is bidding for a slice of the action in fast-growing, more premium ends of the market from Greek yogurt to wholegrain snacks.

But will these US-focused strategies pay off, or do the nation’s top CPG (consumer packaged goods) firms have to put more eggs into emerging market baskets to generate the kind of growth shareholders demand and remain in the global CPG premier league?

‘If you’re not already in the BRIC markets, it’s going to be very hard to catch up unless you make a game-changing acquisition’

One firm attempting to answer this question is global consulting firm OC&C Strategy Consultants, which has been following the fortunes of the world’s top 50 CPG companies for 10 years.

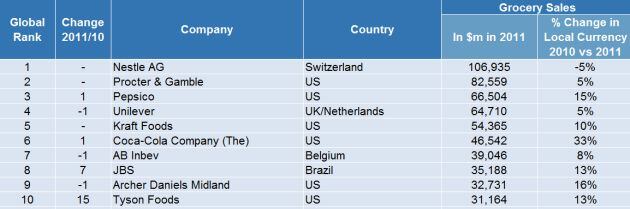

The latest Top 50 index (which is based on 2011 financial data, and will be followed by a new index based in 2012 data in this summer), includes 19 US-based firms, six of whom are in the top 10 (P&G, PepsiCo, Kraft, Coca-Cola, ADM and Tyson).

But will US companies still dominate this index in 5-10 years’ time? And have they been as aggressive as the top CPG players from other countries in Europe, China and Latin America in building international sales?

The US’s historical leadership position in our index has been eroding

While some US-based companies in the OC&C top 50 such as Coca-Cola and PepsiCo now generate a large percentage of sales from emerging markets, many others (General Mills, ConAgra, Kellogg, Dean Foods, Tyson and Smithfield) still derive the majority of their revenues from the US and Europe (although Gen Mills’ $857m acquisition of Brazilian food manufacturer Yoki and Kellogg's recent snacks JV with Chinese giant Wilmar suggests strategies are changing).

“The US’s historical leadership position in our index has been eroding, mainly driven by the emergence of new entrants from the emerging markets” Rambaut Fairley, associate partner at OC&C, tells FoodNavigator-USA.

“This underperformance has in part been driven by US giants’ over-reliance on their home market.

“Those who have been successful in new markets have done so by creating localized products, developing flexible business models, and increasing M&A activities. In particular, leading US players have had success in Brazil and Russia.”

If you’re not already in the BRIC markets, it’s going to be very hard to catch up unless you make a game-changing acquisition

However, in search of the next wave of expansion US players appear to be falling behind, he claims. “For example, Africa appears set to be the next growth engine for global CPG giants, and US companies are currently underrepresented

“This has begun to allow players from other regions, particularly the emerging markets to reach out for global scale. I expect that in five or two years’ time, there will be several more players from China, Brazil and possibly India appearing in the top 50, and fewer US companies.”

Indeed, some of the big US CPG players could themselves become acquisition targets for some leading Chinese firms such as Bright Food Group, Wahaha and Tingyi (sure to feature in the top 50 based on 2012 data), or major Brazilian firms (JBS #8, Brasil Foods #23, Marfrig Group #32) in the future, he predicts.

So have some of the top US CPG players missed the boat, or can they still get a slice of the action in some of the faster-growing markets?

“If you’re not already in the BRIC markets, it’s going to be very hard to catch up unless you make a game-changing acquisition”, says Fairley.

It’s easier to build global brands in beverages and personal care than foods

On a practical level, of course, it is undoubtedly easier to build global brands in tobacco, booze, personal care & beauty, household goods and soft drinks than it is in foods, where tastes are more local, acknowledges Fairley.

For example, Unilever - which wants to earn as much as 75% of its total revenues from emerging markets by 2020 (vs 56% today) - has been steadily offloading food brands that only have national potential (such as Skippy) and investing more in personal care/household brands with global potential (Dove, Cif, Axe etc).

There are exceptions to the rule of course, with snack brands having greater global potential, and some food brands such as Unilever’s Magnum performing exceptionally well in markets from Indonesia to Thailand (Magnum is now sold in more than 50 countries), says Fairley.

However, if you want to build a presence in foods in certain regions of Africa, India or China, you may have to start by acquiring local players and domestic brands - especially in categories such as dairy, meats and bakery - before introducing the locals to JELL-O, he adds.

Click here to read part two.