Speaking on a webinar outlining the findings of its annual food & beverage study – based on a survey of 1,000 consumers – TABS Analytics CEO Dr Kurt Jetta said that just 4.5% regularly purchased food and beverages online, and that online food shopping still accounts for a tiny fraction of overall sales, whereas other product categories have shifted online much more rapidly.

“Online grocery has been around just as long as those other categories [eg. babycare, premium cosmetics, vitamins], which are succeeding, while grocery is failing.”

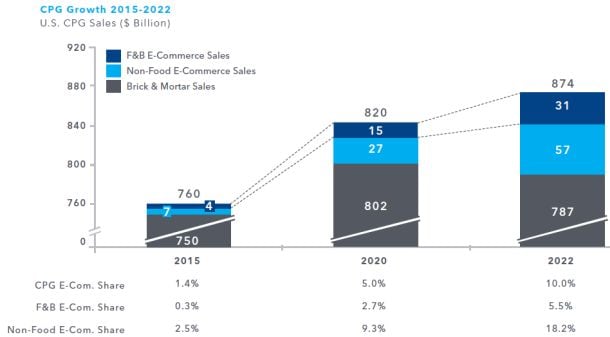

His comments came as IRI released a report estimating that online food and beverage sales accounted for just 0.3% of food and beverage retail sales in 2015 and are predicted to account for 2.7% in 2020 and 5.5% in 2022 (whereas online CPG sales accounted for 1.4% of total CPG retail sales in 2015, and are predicted to account for 5% in 2020 and 10% in 2022).

Dr Jetta: ‘The numbers are horrible’

And while AT Kearney said in a Feb 2016 report that online grocery "is a market poised for dramatic growth," Dr Jetta argued that the "numbers are horrible."

He added: “For the fourth year in a row, consumers have turned their backs on buying groceries online no matter how much online grocery retailers try to entice them. 69% of consumers never buy groceries online. With only 15% of consumers stating loyalty to shopping for groceries online, this is not a sustainable business model, especially when you consider the industry loyalty rate benchmark is 70%.

“Food companies and grocers need to figure out why there is such a high level of dissatisfaction with the online channel before they continue to invest any further in it. Amazon is going up but if you look at the other grocery banners and the percentage of respondents purchasing online by outlet, they’re going down.”

He added: “Why did Target get out of curbside pickup? Our data suggests that there is no demand for it. Still only 1% of the population is doing it regularly.”

'Purchase frequency is high, units per transaction is high and cost per unit is low...'

In a follow up blog post, Dr Jetta added: “Why does online have to completely ‘disrupt’ grocery just like it has other sectors? TABS studies have shown that that the online channel performs very well in the Baby, Vitamin and Premium Cosmetics categories where the purchase frequency is low, items per transaction are relatively low and the item cost is high. But the dynamics for grocery are just the opposite: purchase frequency is high, units per transaction is high and cost per unit is low.

“Online Grocery has been around just as long as those other categories, which are succeeding, while grocery is failing.

“Target is shutting down curbside, Wal-Mart is not releasing online figures except to say that they are slowing down, and there is general recognition that Peapod has been online for two decades and has yet to gain any major market share traction and profitability.”

He added: “As it stands, there are no facts to suggest that a massive boom from this channel can be expected any time soon, or ever, really.”

Many brands are succeeding online

But isn’t this a bit of a sweeping generalization, given that there are many different online shopping models utilizing very different approaches, some of which appear to be doing better than others?

For example, some involve picking from dedicated fulfilment centers/warehouses, others from stores; some involve delivery; others curbside pickup; and others, such as InstaCart and Google Express, utilize existing infrastructure and recruit personal shoppers to pick and deliver orders from stores in their own vehicles – a service that upmarket retailer Andronico’s claims has brought in a significant amount of incremental business (Instacart has also done deals with Whole Foods, Publix, Target and Costco).

Kroger, which has partnered with InstaCart in Georgia, recently expanded its ClickList service to multiple markets.

It has also been testing Vitacost.com's technology and ship to home infrastructure in Denver through a pilot in King Sooper's and has been testing an ‘endless aisle experience’ in its Main & Vine store in Washington.

Meanwhile, Whole Foods' co-CEO Walter Robb said on the latest earnings call that he felt "really good about the partnership with Instacart and the results we're seeing," while InstaCart CEO Apoorva Mehta told delegates at the TechCrunch Disrupt conference that InstaCart will be "cash-flow positive" in the next 12 months.

(Perishables - products many consumers say they are wary about purchasing online - are also among InstaCart's top-performing categories, according to AT Kearney.)

Many specialty food firms are also using online platforms enabling manufacturers to deliver direct to consumers via drop shipment (DirectEats) or warehouses (Thrive Market), while many also claim to be generating strong sales directly via their websites or via other online platforms (Quest Nutrition, EXO, Soylent, Enjoy Life Foods).

Meanwhile, some ‘farmers market on wheels’ type operations such as Door to Door Organics claim to be expanding profitably.

Dr Jetta conceded that some brands are succeeding online. But he added: “Quest Nutrition is the poster child of the successful online brand, and baby products and vitamins do well, but for whatever reason, people don’t want to go online regularly to buy groceries. It’s the emperor with no clothes.

“Online grocery [retailers] have to pick orders and ship them to your house, two fundamental costs that are currently being subsidized by consumers in bricks and mortar stores. If any of the [major grocers] were making any money [from online sales] they would have to state it [in their financials]."

"As we conducted the study [a July 2015 survey of 1,341 grocery shoppers, 90% female] it quickly became clear that this is a market poised for dramatic growth. More than a third of primary grocery shoppers have purchased groceries online over the past 12 months, a sizeable increase from last year. Moreover, the movement online is led by shoppers from particularly attractive segments - urban dwellers, millennials, and those earning >$75k/year."

AT Kearney, Capturing the Online Grocery Opportunity, February 2016

Nielsen: ‘Online CPG sales are growing 20% annually, outpacing brick and mortar retail growth by three times’

So what do other market watchers say?

Jim Hertel, managing partner at retail analytics firm Willard Bishop, told FoodNavigator-USA that while online grocery's market share is very low today, he remains convinced it will grow significantly: “We are more bullish [than TABS Analytics], and there are a lot of fundamental reasons why we think it will grow to ~10% of sales in 10 years or so. That doesn’t sound all that big until you calculate the entire market at $1.3 trillion, so even 10% is real money.”

Jordan Rost, VP consumer insights at Nielsen, meanwhile, told us that he was equally optimistic: “While consumers are only spending a low single digit percentage of their CPG dollars via digital channels today, we expect that share to grow rapidly over the next 10 years.

“Overall, online CPG sales are growing 20% annually, outpacing brick and mortar retail growth by three times. Over the last three years, shopper consideration for online purchases of consumer goods has also more than tripled. As more touchpoints along the path to purchase happen on digital platforms, and as the number and variety of experiences offered by these platforms grow, we expect more consumers to take advantage of these new offerings.”

IRI: Online CPG sales set to rise from $11bn in 2015 to $88bn in 2022

IRI, meanwhile, predicts that total CPG dollar sales via e-commerce will jump from $11bn in 2015 to $88bn in 2022.

“Amazon, for example, has scaled home shipment with Prime and Prime Pantry for non-food and shelf-stable food and beverage and is testing time-window home delivery with AmazonFresh. The retailer has launched and is scaling immediate home delivery with Amazon Prime Now, is testing click and collect with Amazon Locker and has plans to launch two drive-up stores in Silicon Valley.

“Walmart is also testing food and beverage home delivery... has scaled click and collect for non-food and shelf-stable food and beverage, and is scaling fresh, refrigerated, and frozen click and collect across markets.

“Ahold is investing heavily in Peapod to scale out the home delivery company it purchased years ago. It has also been testing click and collect in suburban markets."

IRI also highlighted the success of Quest Nutrition [a presenter at Food Vision USA in Chicago this November], which it says, “has successfully synchronized in-store and e-commerce efforts, including big events like its 'Cheat Clean' campaign, and 'Quest Food Trucks,' which have resulted in a sales increase of 77% year-over-year and a 48% share capture of the e-commerce snack bar market versus an 8% instore share capture.”

What’s the size of the online grocery shopping prize (and how reliable is the data)?

According to a new report on omni-channel shopping from IRI, online CPG sales accounted for 1.4% of total CPG retail sales in 2015, and are predicted to account for 5% in 2020 and 10% in 2022 (compare this with AT Kearney’s slightly more bullish predictions of a 12-16% share for online grocery in 2023).

Online food and beverage online sales meanwhile, accounted for just 0.3% of food and beverage retail sales in 2015 and are predicted to account for 2.7% in 2020 and 5.5% in 2022, said IRI.

But how is IRI’s data calculated, given than many players in this space are privately held and do not publish sales, and that many publicly listed players such as Walmart and Kroger do not break out online sales in their financial results?

According to IRI principal Greg Konczyk: “IRI leverages shopper data from multiple sources including (1) National Consumer Panel (NCP), (2) ReturnPath, and (3) comScore, as well as (4) direct e-POS data from retailers where available. Additionally, we source attitudinal shopper data from periodic e-commerce-focused surveys that we conduct with the NCP. Our e-commerce data partners provide transaction-level detail from shoppers participating in their panels, and these sources track and provide data for over 500 selling domains (including all major CPG e-retailers). The overall number of shoppers in our data sources (across the US e-commerce universe, not limited to CPG) is over 2 million.”

He added: “We utilize a panel-based consumption model based on IRI’s custom developed IP and leveraging access to multiple consumer data partners, who provide transaction level detail to develop a significant consumption-based sample. Use of consumption-based models are not necessarily optimal for market measurement tracking, however, they are the best acceptable options, when major retailers/websites such as Amazon and Walmart.com have determined they do not wish to share e-POS data at this time.

“We believe that a combination of the most comprehensive ecosystem of data assets, retailer and data provider partnerships, and IRI’s proven and tested data science methodologies allow us to create an industry leading portfolio of e-commerce solutions delivering valuable insights to our stakeholders.”

IRI works with manufacturers to identify how shoppers are interacting with their brands along key touchpoints, says the Chicago-based market research firm, which describes how this benefited one CPG client:

“Through a survey and an in-store versus e-commerce product assessment, IRI identified that the shoppers on Amazon were looking for new products and flavors, while Walmart.com and Peapod shoppers wanted the same product, but wanted the convenience of not going to the store. With this knowledge, the brand was able to optimize its distribution strategy, pushing all SKUs on Amazon and using it as an 'innovation playground,' while pushing the top SKUs at Walmart.com and Peapod.”