Trader Joe’s is most at risk from Whole-Foods/Amazon: Magid expert

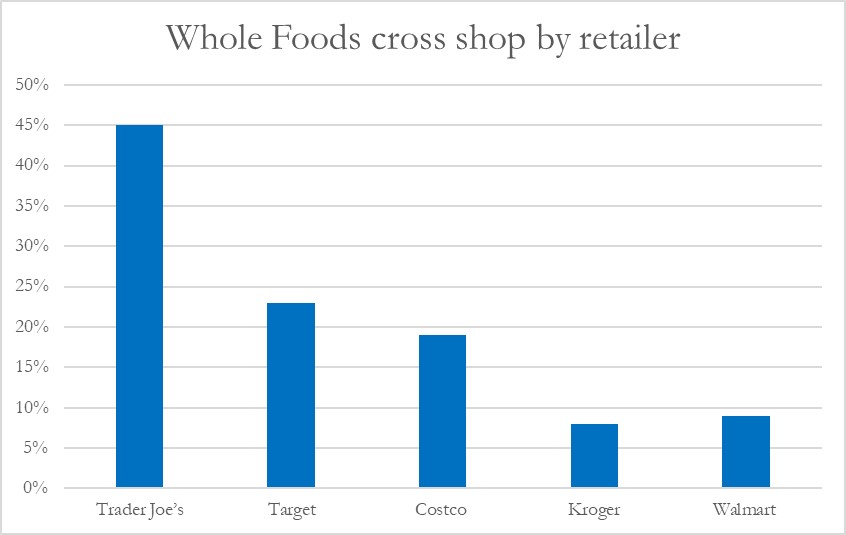

While many retailers are concerned with the impact of Amazon on grocery pricing, the threat to Trader Joe’s has little to do with price changes, said Matt Sargent, Senior Vice President of Retail at Magid. The big risk to Trader Joe’s is because its customers aggressively cross shop at both Whole Foods and Amazon at levels three to four times the industry average (see figures below), according to Retail Pulse data from Magid.

“The risk is much less for a Kroger or a Walmart,” Sargent told us. “Yes, Walmart is making changes to compete, and Costco is, but Trader Joe’s is the most at-risk retailer. I would imagine that many Trader Joe’s consumers were once Whole Foods consumers who migrated due to pricing or convenience.” Those consumers may now be returning to Whole Foods.

Data from The Thasos Group supports this observation, with Trader Joe’s experiencing the highest rate of customer defection to Whole Foods at 10%, followed by Sprouts at 8%. On the other hand, the largest percentages of Whole Foods’ new customers in the week after the price reductions were announced came from Walmart (24%), followed by Kroger (16%) and Costco (15%).

The price issue

Amazon announced a raft of price reductions across a range of best-selling staples across its stores, including bananas, avocados, brown eggs, salmon and tilapia, baby kale and baby lettuce, ground beef, almond butter, some apples, rotisserie chicken, butter, and more.

This led to a 25% boost in customer foot traffic in Whole Foods, according to widely reported data by Foursquare Labs Inc., which pulls data from consumers’ mobile devices.

Amazon also moved quickly to add Whole Foods private label items to its Prime Now and Prime Pantry platforms post-acquisition, and notched up sales of almost $500k in week one. The company ran into inventory issues pretty rapidly after underestimating demand.

However, those initial price reductions may have been short-lived with analysis by Gordon Haskett revealing that prices for a basket of 110 items at a Whole Foods store in Princeton, NJ had not really changed from August 28 (the day when Amazon officially took over) and September 26. The analysis showed that 77 of the 110 items remained the same, with decreases noted for 17 and price increases reported for 16 items. Amazon has not made any firm commitments about longer-term price cuts at Whole Foods stores.

The Thasos Group reports that the price reductions did not attract a lower income demographic to the retailer and, “the defecting regular customers from each competitor represented the wealthiest segment—with income levels comparable to Whole Foods’ regular customers--of their respective customer bases” (according to an October 3 Competitive Impact of Lower Prices at Whole Foods analysis.

According to Packaged Facts, Trader Joe’s attracts 10.5% of US adults as customers, compared with 6.3% for Whole Foods (defined by the number who shop there at least once a month).

The 10-year compound annual growth rate in customer base for Trader Joe’s is 5.9%, compared to 4.9% for Whole Foods. In comparison, Kroger’s 10-year customer base CAGR is 0.2%.

“But notwithstanding the multi-decade phenomenon of Whole Foods and Trader Joe’s, the natural channel remains a fragment of food retailing overall. The U.S. grocery retailing business has never been more competitive, and this may be especially so for retailers featuring natural and organic foods,” states Packaged Facts.