What is happening in the coconut water market?

One of the most thought-provoking sessions was presented by Brian Reed from IRI and Kathryn Peters from SPINS, who revealed that in the 52 weeks to September 28, 2014*:

- Dollar sales of ‘clean-energy’ beverages grew 64%

- Dollar sales of kombucha grew 50%

- Dollar sales of veg juice & blends grew 46% (representing a "huge resurgence", driven by premium brands such as Suja and growth in ingredients such as beet and kale)

- Dollar sales of ginger beverages grew 17%

- Dollar sales of ready-to-drink coffee grew 12%

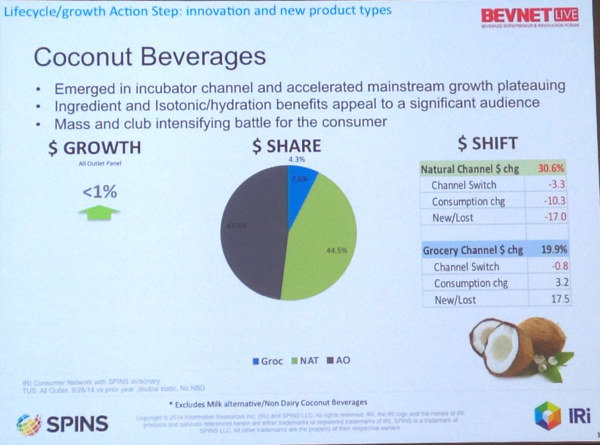

- Dollar sales of natural coconut beverages (broader than just coconut waters, but excludes coconut water coffees and dairy alternatives such as So Delicious) grew less than 1%

- Dollar sales of ready-to-drink tea were flat - but new products such as Runa are attracting new consumers to the category.

Vita Coco: Our sales are up 30% YoY

The coconut water statistic - not surprisingly - generated the most debate. Asked for its take, market leader Vita Coco told FoodNavigator-USA: “When we focus on coconut water’s activity in supermarkets, mass/club outlets and c-store, the category is actually seeing around 22-25% growth. Vita Coco’s sales trend higher than this average, approximately 30%. For any maturing category or brand to show this kind of growth is impressive.”

A spokesman added: “In addition to Vita Coco’s continued strong growth in the U.S., the brand is enjoying even stronger growth in Europe and other new markets, some as much as 200%. Coconut water remains a trend-leading beverage category with untapped sales potential in North America and abroad.”

SPINS: Move to the mainstream has put pressure on prices

Asked to clarify how Vita Coco's bullish assessment of the market squared with the data shown to BevNet delegates, Mary Ellen Lynch, director of consumer insights & strategic partnerships at SPINS, told FoodNavigator-USA that the unit sales growth figure would be higher than the dollar sales figure.

”The mainstreaming of the segment is putting downward pressure on price which also contributes to the flatter growth. Also, we did validate against POS trends prior to including in the presentation.”

So has SPINS had any feedback from the trade about the data? SPINS was “approached by two strategic consultants that expressed that the SPINS information was ‘on target’, she claimed.

“We also received feedback from two significant coconut water manufacturers, the smaller of which whose leadership did not believe the SPINS story.

"However the larger brand stated: 'It’s not surprising to see a flatter number across all outlets. The shifting of buyers and volume from natural & specialty retailers to mainstream aligns very closely with POS trends, with the category slowing down to low double digit growth in Natural/Specialty Gourmet Channels. Your point about a category needing innovation in order to maintain growth is right on. HPP (high pressure processing) and brands like Harmless Harvest are great for the category and we definitely expect them to scale. The cold-chain route to market is also a big point of differentiation.' "

Harmless Harvest: Gong back to category's premium roots

Harmless Harvest, which picked up the BevNet Best of 2014 ‘Product of the Year’ award for its raw organic coconut water (treated with HPP rather than flash pasteurized), has “managed to add a premium layer to a product that had already established itself at a premium price”, according to BevNet.

“With new offshoots in tea and chocolate, innovation continues to roll out of the company, but it’s actually a focus on the core brand that has raised the bar for the industry from a product and purpose point of view.”

* The data covers the 52 weeks to September 28, 2014, vs the previous 52-week period and is all-outlet IRI shopper network data with SPINS attribution and universal product codes unique to the natural channel, so brings in a "much wider universe than would normally be included in POS-based reporting", according to SPINS.