Dr Kurt Jetta, founder and CEO of CPG analytics firm TABS Group, told FoodNavigator-USA that while the combined entity would have significant clout with suppliers and retail/foodservice customers, and Kraft would be able to expand its geographical footprint via tapping into Heinz’s global distribution network, their alliance was forged from weakness, not strength.

Neither firm is really growing, he pointed out, with Kraft chairman John Cahill noting in February that the world is changing – but Kraft is not keeping pace, while a March 13 SEC filing from Heinz revealed that despite its significantly improved margins (following aggressive cost-cutting), sales slumped 4.6% in 2014 as consumers were uninspired by its frozen meals and potato products.

The outlook for innovation is even worse as brands will get even less focus

He added: “It’s almost as if the large tier one guys have surrendered. They know that the status quo is impossible, that they have to keep driving value for shareholders, but they don’t know what to do. You only had to listen to Tony Vernon [former Kraft CEO who left in December 2014] in the earnings calls last year. It was like he was just helplessly throwing up his hands.

“They have become so big that they just can’t respond to the consumer without pretty radically changing the way they do business, but they can’t do that, so they have to make acquisitions - because they certainly aren’t growing their top lines organically - engage in ruthless cost cutting, or divest things.”

But getting even bigger – which means individual brands will get less focus – is not a winning strategy for revitalizing brands, he said, while all the evidence points to the fact that bigger isn’t better when it comes to driving top-line growth in the CPG market.

“The outlook for innovation is even worse as the brands will get even less focus.”

You can cut costs for a couple of years but ultimately, long term growth has to be facilitated by revenue growth

As for scale, it boosts buying power and may increase leverage in negotiations with customers, but it doesn’t drive innovation, he added.

“One of the biggest under-reported trends in the industry is how significant the lag is from the top tier one manufacturers and everyone else. There’s about 20 firms that each do at least $5bn in retail revenue a year and account for 34% of industry sales, but their CAGR [compound annual growth rate] over the last five years is 0.6%, whereas the industry CAGR over the same period was 2.1%.

“They have lost share each of those years and the growth is really coming from tier three, tier four – companies doing around $50m to $200m, $250m.”

Cost-cutting, meanwhile, only delivers short term gains, he said: “You can cut costs for a couple of years but ultimately, long term growth has to be facilitated by revenue growth, but they are not nimble enough to innovate and align with changing consumer tastes – these big companies just come up with line extensions and flavor variants but really nothing revolutionary.”

He acknowledged that Heinz had recently launched yellow mustard and Jalapeno and Sriracha ketchup to appeal to US Millennials, along with hotter, spicier sauces in Europe, but added: "If you think of the biggest innovations, it's really the upside-down bottle, but that was quite a long time ago."

Is a mega-merger better than radical portfolio reshaping?

So what should huge CPG companies do instead, if mega-mergers won’t deliver long-term topline growth? Radically realign their portfolios by divesting under-performing/tired brands and use the proceeds to vacuum up smaller, faster-growing companies?

Possibly, said Dr Jetta, who acknowledged that there have been a series of such acquisitions recently, from General Mills’ deal to buy Annie’s, to Unilever’s purchase of Talenti to Pinnacle Foods’ acquisition of Gardein.

But given the sheer size of Kraft and Heinz, buying up natural or organic companies doing tens or even low hundreds of millions of dollars doesn’t make a material dent in your overall performance, he said. “These kinds of deals would be inconsequential, and they don’t create shareholder value in the short term."

Morningstar: We’ve thought for some time that Jell-O could be axed

However, Morningstar analyst Erin Lash, was more upbeat, noting that the deal “stands to boost the competitive positioning of the combined entity”, increasing the firm’s leverage with customers, while it would also “extend the distribution of Kraft’s fare across Heinz’s vast global distribution platform”.

As for portfolio restructuring, she also predicted that several underperforming brands might get the chop post the deal, while it was also possible that “the firm’s new management could look to build a more notable presence in the natural and organics aisle.”

She added: “We’ve thought for some time that Jell-O – which continues to falter despite multiple stabs at putting it on more stable ground – could be axed in favor of allocating more capital to faster-growing categories such as organics, or even pursuing a tie-up outside the US.”

And while Kraft has not set the world on fire with breakthrough innovation, it had made solid progress in recent years, she claimed, noting that “revenue from innovation increased to around 14% [in 2014], more than two times the level generated in 2009, which we view as an impressive turnaround.”

HOW ARE THE BRIDE AND GROOM DOING?

HEINZ: Group sales fell 4.6% to $10.92bn in 2014, while sales in North America fell 6.3% to $4.25bn, which Heinz blamed partly on “category softness” in the frozen meals market [Smart Ones] and “share losses in our frozen potatoes [Ore-Ida], meals and snacks businesses”. Sales in Europe fell 1.7%, sales in Asia-Pacific slumped 9.6%, while sales in Latin America rose 3.6%.

On the plus side for its private equity owners 3G and Berkshire Hathaway, who have been aggressively cost-cutting since the deal to take Heinz private closed in June 2013 (Heinz has closed or announced plans to close factories in the US, Europe and Canada, and slashed 7,400 jobs between April 2013 and December 2014), EBITDA margins surged from 18% to 26% [Source: 10-K filing, March 13, 2015]. It has also sold Shanghai LongFong Foods in China and its domestic foodservice frozen desserts business.

KRAFT: Net revenues fell 0.1% to $18.205bn in 2014, which CEO John Cahill described as a “difficult and disappointing” year: “It's clear that our world has changed, and our consumers have changed, but our company has not changed enough, and certainly has not kept pace.”

Kraft’s organic net revenue growth of 0.9% trailed North America food and beverage industry growth of 2%, he added: “In 2014, we did not grow share in any individual category. We merely held flat at 60% of our US businesses, and lost share in the other 40%.”

However, some innovations had delivered: “Oscar Mayer P3, McCafé coffee and the rejuvenation of our Philadelphia soft cream cheese line have all been well received.”

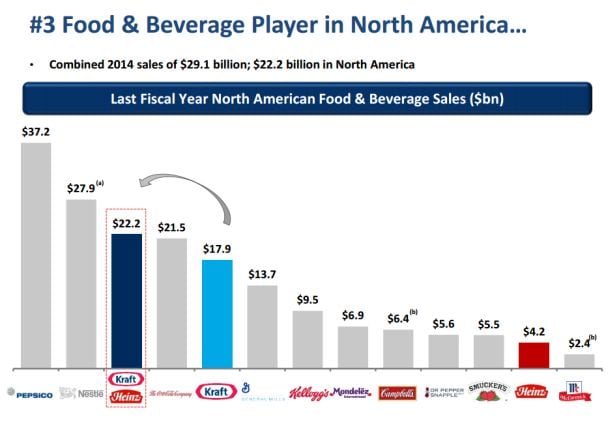

HOW BIG WILL THE NEW COMPANY BE? The combined entity would leapfrog Coca-Cola to become the third largest food and beverage firm in North America behind PepsiCo and Nestlé with $22bn+ in North American sales, and the fifth largest food and beverage company in the world with $29bn+ in global sales.

GEOGRAPHICAL FOOTPRINT: While most of Kraft’s sales are in North America, 61% of Heinz’s sales are generated from outside this region, and 25% are from emerging markets, providing opportunities to take Kraft brands into new markets. Analysts at ECRM data also note that Heinz could increase its presence in the drugstore channel by teaming up with Kraft, which has a much stronger foothold there.

SYNERGIES: Bosses say they expect to realize $1.5bn in annual cost savings by the end of 2017.

BRANDS: The combined entity will include Heinz Ketchup, Classico, Ore-Ida, TGI Friday’s, Weight Watchers, Heinz Beanz, and Smart Ones; plus Kraft, Velveeta, Jell-O, Oscar Mayer, Philadelphia, Cool Whip, Kool-Aid, Capri-Sun, MiO, Planter’s, and Lunchables.

STRUCTURE: The new company will retain offices in Chicago and Pittsburgh.

MANAGEMENT: Heinz CEO Bernardo Hees will be CEO of the combined company, while Kraft CEO and chairman John Cahill will be vice chairman.