Logically, scale should bring advantages, Dr. Krishnakumar (KK) Davey, managing director at IRI Consulting, told FoodNavigator-USA. More purchasing power; more category clout with retail customers; superior economies of scale; and the ability to hire the best talent and the hippest ad agencies.

However, a new analysis of more than 400 leading US CPG manufacturers reveals that the larger players are not outperforming their smaller rivals, in fact quite the opposite, said Dr Davey.

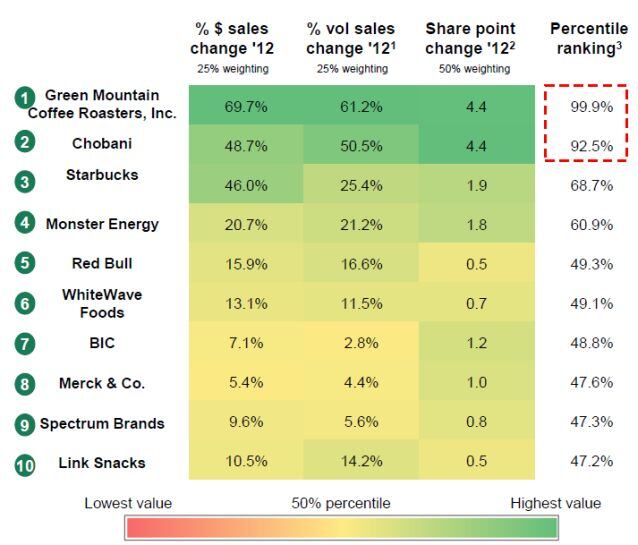

“We divided the companies up into three groups: Those with retail sales of $100m to $1bn, those with retail sales of $1-5bn and those with retail sales of $5bn+.

“We then assessed them using three metrics: dollar sales growth, volume sales growth and market share gains. We then ranked the companies and found that the small and mid-sized firms were more likely to be growing all three (sales, volumes and market share)."

Price is not a lever you can just keep pulling

He added: “Everyone knows that smaller companies can be more agile, and that retailers like working with some smaller manufacturers that can help them differentiate themselves with unique products.

“But we were surprised by the discrepancies between large, medium and small companies that we found. It seems that smaller manufacturers are really taking a slice of growth away from big manufacturers.”

Indeed, very few $5bn+ CPG companies are systematically driving dollar sales, volume sales, and market share, he said.

"The larger players increased dollar sales by putting up prices early last year to cover rising costs, but this is not a lever you can just keep pulling.

“Midsize winners are growing their base business through distribution and velocity, increasing consumer buy rates significantly and capitalizing on consumer macro trends; and small winners are showing the largest dollar and volume growth rates and the largest share gains.”

Small and midsize companies are increasingly taking market share from large competitors

Indeed, all top 10 small and midsize companies in the BCG/IRI ranking gained market share in 2012, with eight of the small-company winners grabbing at least 1 percentage point. Yet since 2009, large companies as a group have ceded 1.4 points in market share, a drop that amounts to more than $10bn in lost sales, he added.

“Small- and midsize-company winners are generally concentrating on a few product categories in which they have a competitive advantage and experience strong consumer demand. They are also driving trends in the marketplace and developing first-mover advantage.”

PepsiCo: Decline is not inevitable in every mature low-growth category

But while many leading CPG players are now pumping all available resources into faster-growing emerging markets, firms such as PepsiCo are not ready to throw in the towel in mature markets just yet, he said.

Indeed, PepsiCo CEO Indra Nooyi recently spelled this out in the firm’s Q1, 2013 earnings call, in which she argued that established players such as PepsiCo should "reinvent" mature, low growth categories such as carbonated soft drinks instead of letting others step in and do the job for them, noted Dr Davey. (Click here for details).

Similarly, large players such as General Mills are using their R&D expertise to re-engineer existing product portfolios in a healthier direction, as well as snapping up smaller companies that have exploited faster-growing market niches, he said.

Coca-Cola, meanwhile, has used its Venturing and Emerging Brands arm to help it identify the right horses to back in the North American beverage arena, as well as seeking out new opportunities in developing markets, he added.(Click here).

“There is no single formula for success in the CPG marketplace.”

Hartman Strategy: Meet the needs of upscale shoppers, and growth will follow

But what categories are the sexiest in the current food retail landscape?

According to Hartman Strategy, the consulting arm of trend-watcher Hartman Group, growth has consistently been at the premium end of many categories from energy drinks to single serve coffees, Greek yogurt, ready-to-drink teas and protein shakes.

And counter-intuitive as this may seem in the current economic climate, manufacturers most attuned to the tastes of a small but powerful group of affluent and educated ‘upscale’ shoppers are the most likely to succeed in the broader marketplace, according to senior VP James Richardson.

The influence that foodies and 'upscale' shoppers have over food culture - and the choices made by ‘mid-market’ shoppers - is disproportionate

Speaking to us in February, he said: "This slice of America is a distinct social world whose internal lifestyle movements - fitness, endurance athletics, health and wellness, immersive foreign travel, foodiedom - have created some of the most intense and defining cultural aspirations of our time.”

And while the overall numbers of ‘upscale’ shoppers are small, the influence they have over food culture - and the choices made by ‘mid-market’ shoppers - is disproportionate, he added.

“The absolute size of the upmarket prize is less the call to action than the enormous scale of their influence on the mid-market consumer, whose taste preferences continue to alter upward in terms of quality expectations, especially related to health and wellness."

Click here to read part one of our special feature on the OC&C Index of the world's 50 top CPG companies.

Click here to read part two.