While this suggests that food brands have held their own against private label in spite of the recession, recent analysis by the Hartman Group reveals that the story is much more complex—with a huge variance in PL share by category relating to how brand culture shapes consumer receptivity to store brands.

Unlike Europe where private label share is approaching 50% in some markets, the US PL market remains hugely fragmented, as the Hartman Group noted in Hartbeat Exec: The Future of Private Label Food.

Private label dollar share has been essentially flat since 2008—hovering around 16%—even though total PL share across grocery continued to grow until 2011. The leveling off suggests that food brands have withstood the shift in favor of private label among previously light PL buyers in the wake of the economic downturn of 2008, as the market researcher noted.

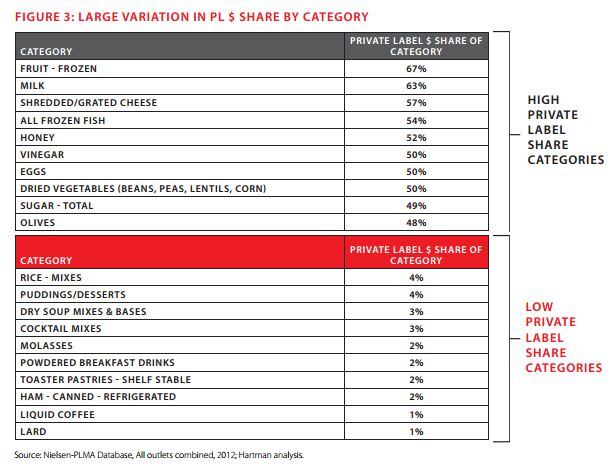

Moreover, PL share and share growth by category has varied enormously, with certain categories (such as frozen fruit and milk) exhibiting 60+% share going to private label. Nearly 20% of categories (27 out of 150) exhibit twice the average PL dollar share.

Still, shares of categories such as rice, dry soup mixes and liquid coffee have remained marginal (at 4% and below) during that same period. Indeed, more than half of packaged foods’ major categories have demonstrated flat PL share growth from 2009 through 2013—the same time period when economic theory would suggest PL share should be edging up generally, Hartman Group noted.

Through its analysis, the firm broke the private label marketplace into four segments: PL’s growth engines, PL’s roots, battleground categories and branded fortress categories.

Growth engine categories: consumers make the food experience, brand affinity is low

The growth engine categories—including cheese, chilled ready meals, olive oil, honey, prepared salads and chilled pizza—demonstrated average PL share growth of 3.9% from 2004 to 2013 (compared to 1.4% for total PL) and average share of 29.8% last year (compared to 16.5% for total PL). These products tend to be either dinner ingredients that depend on the home cook to be transformed into meals or fresh perimeter categories that haven’t historically been dominated by brands.

Because consumers see themselves as the makers of the end-food experience, the cultural stakes associated with ingredient purchases are lower than for ready-to-eat or value-added prepared foods. Moreover, the historical dominance of retailers in fresh perimeter commodity categories means name-brand affinity isn’t a big factor, though the growing popularity of value-added categories means the perimeter could become more branded than it is today.

Where PL share dominance began (but can it be sustained?)

Despite below-average growth of 0.5%, the roots category—comprising frozen potatoes, canned tomatoes, canned fruit, frozen vegetables, butter and chilled soup—controlled 34% of category share in 2013. This segment, anchored by processed commodities, forms the traditional core of the private label market.

Consumers traditionally perceived little differentiation between the PL and legacy branded choices in these categories, though the declining topline situation in some suggests that doesn’t necessarily mean they like the food. Indeed, many of these categories will likely decline as consumers turn to fresh or shelf-stable “out-of-the-can” alternatives. The categories that are growing well (butter and nuts) suggest that PL has maxed out its ability to drive differentiation through imitation, and that future growth will likely be on the upmarket side.

Battleground: where price promotions are king and brands have the ‘trust’ edge

As products get further from staple ingredients and implied cooking, consumers’ affinity for brands tends to rise, Hartman Group found. From chilled lunch kits and chips to frozen pizza, canned soup and table sauces, the battleground category is where many CPG power brands aren’t afraid to run aggressive price promotions, marketing, product proliferation and slotting fees to maintain market share. Indeed, while average category PL share growth in this category exceeded total PL (4.6% for 2004-2013 vs. 1.4%), average PL share in 2013 was 9.7%, notably below the 16.5% average.

As consumers have historically not trusted grocers to cook dinner for them or make their snacks (though this appears to be changing), brands have become critical culturally as a trust builder and authenticity cue. These categories also have strong premium segment sales driven by upmarket entrepreneurial activity, which reinforces brand power at the shelf. Still, PL share is rising here, as better-quality snack innovations allow consumers to save on high-consumption rate categories like chips, popcorn and extruded snacks, and the low barrier to entry enables PL to steal share from value-added meal categories with already weak brands (e.g. frozen pizza).

Branded fortress: strong brand heritage, declining categories

Faced with below-average dollar share (-1.6% from 2004-2013) and share growth (6.2% vs. 16.5% in 2013), the private label categories associated with indulgence and highly intentional functional snack occasions are actually losing ground to brands. In order to ensure they’re getting the highest-quality product, consumers seek out brands as category specialists in categories including frozen ready meals, yogurt, dips, breakfast cereal, margarine and dinner mixes.

For these categories, strong brand heritage and fairly low price points make remaining consumers reluctant to switch to private label permanently. Not only that, but declining center-store categories suffering long-term decline (e.g. breakfast cereal, spreadable oils and fats, dried ready meals and frozen ready meals) mean the likelihood of huge market share gains for private label is slim.

What’s the future of private label?

The future of private label food’s growth depends largely on premium innovation in PL products and how much the PL retail model will actually expand in the US, Hartman Group says.

Trader Joe’s and ALDI, with 395 and 1260 stores respectively, represent the most aggressive invasion into the brand-dominant grocery store model. Their popularity (ALDI’s as an incredibly cheap alternative and Trader Joe’s as an experience-driven alternative with just plain “cool” products) has shown that consumers might not care as much about brands as they’ve traditionally thought. This could prove troublesome for legacy brands in the battleground and fortress segments, especially in value-added packaged food.

Recent major natural private label launches in Safeway (Open Nature), Walmart (LifeChoice) and Kroger (Simple Truth) no doubt demonstrate a turning point for premium private label credibility. Indeed, the strategy to simulate a name brand as a strategy to move upmarket relative to typical private label pricing shows promise, though it’s early to tell. Hartman Group maintains that it will be hard for retailer-exclusive control labels to be perceived on the same level as a name brand to the consumer and to perform financial like successful CPG brands.

“The winners in premium control label will either go narrow and deep in a few adjacent categories or simply take over the store with a well-define premium proposition,” Hartman Group wrote, noting that Walmart’s LifeChoice experiment represents this narrow and deep approach to premium private label—and will be one to watch.

Still, Hartman Group forecasts that private label share will grow in select packaged food categories that are on trend from a consumer perspective (e.g. upmarket, entrepreneurial brands in value-added categories) and where CPG brands can’t maintain the strength of branded price premiums or are uncomfortable (fresh perimeter).